I was inspired by the Bill Holter interview on Palisades Radio the other day to write this. He makes some really good points and discusses some end of days scenarios, but a particular idea caught my attention that drew me towards writing this article in particular. Towards the end of the interview, he discusses how electric companies or the like may operate on a form of credit, and you paying them allows this credit to continue to be extended. What happens if a vast majority of people can no longer pay and they default with their creditors? He mentioned how maybe a bread maker may have 7 or more lines of credit with suppliers. They may make a large order for flour from a supplier, they get the product, make bread, sell it, and pay the creditor. I’m completely oversimplifying, but the concept he mentioned is that is this particular issue – the credit structure itself may be problematic and this can then have problems keeping the lights on in your house or keep bread from being stocked on shelves.

What I had considered was that if I had enough money, I could just pay the bills to keep the lights on or scrounge up enough to buy bread. I hadn’t considered that the supplier themselves would go bust because no one extended them credit. I think our Fed has thought of some of these issues, which is why they are sending direct checks to people. In the 2008 crisis, the Fed gave banks money to lend out – but credit scores were affected and credit tightness kept money from being lent out. The Fed has bypassed this roadblock – and in a sense, became a back stop creditor of last resort when banks won’t lend to you. On a side note, the same thing that kept inflation under check, to an extent, in the 2008 housing crisis – that is, the Fed printed money, but to banks – has been eliminated and now trillions are flowing directly to the people to spend. This helps liquidity problems that were of significance during the Great Depression. When banks don’t lend out due to such high risks of default, the velocity of money stops – and there’s where you get your deflation.

But that being said, I felt there may be a book in this. Honestly, this may have already been done. Also, it may be wayyyy too late to do it as this whole thing can pop any minute. So I wanted to kind of lay out a summary of a book here. I could crank out 50 page papers for my masters degrees, and I can crank out volumes of info here on my blogs in a stunningly short period of time. My high school friends and I used to just bounce ideas off of each other all the time. The twins I was friends with, both have PhDs in microbiology, but one then went crazy and got a law degree as well. One is a well known race horse owner who works for a hedge fund trading futures. One in my circle was the inventor of YouTube. Yeah. To be quite clear, we shared a best friend who was an idea guy, so my and him weren’t exactly hanging out all the time. My point is I came from a background where people shared a lot of ideas. Maybe some were stupid. But it was a factory for people to succeed in this environment. I’m the ugly duckling of the group with 2 master’s degrees, if that puts it into perspective.

OVERALL CONCEPT

By trade, I’m an IT manager. Not going to get into where, but I run a very large organization in disciplines like desktop support, server support, networking, and cybersecurity. In my early days, I was a metrics manager and was tasked with doing a risk analysis for our team. I was to identify the threats, determine their likelihood, determine their impact, and then determine a course of action (COA). In the risk game – you can accept, transfer, or mitigate.

For example, one threat I may have is a hurricane to our operations. While the impact could be severe, the likelihood is extremely low for my location. However, if I lived in Florida, this likelihood would be much higher. Therefore, an IT manager where I am would evaluate that threat differently than one in Florida. In my current location, I may choose to accept the risk and do nothing, or transfer the risk with insurance, or if I lived in Florida, I may have to mitigate it with a hot site several hundred miles away for continuous operations. Each organization would have a different set of threats and risks. And – in the financial risk game going on, each person may have a different likelihood of occurrence for different threats.

There’s a few others, but I’m going to keep this high level. You put this into a matrix, and then prioritize your highest scoring items.

The overall concept is to identify a lot of the risks of the financial system. For example, Holter discussed the credit issues affecting energy to your house. You might buy a generator to mitigate this. Dent talks about deflation, and your mitigation may be to talk with a financial planner about re-balancing your portfolio if you feel Dent is right. Maloney gave a history of money and the big lesson here is debasement of currency – and you can transfer some of this risk with “insurance” in gold. Peak Prosperity got me thinking about a homestead to protect your food supply – therefore you are mitigating your food risks. Section one would be outlining the risks that are out there.

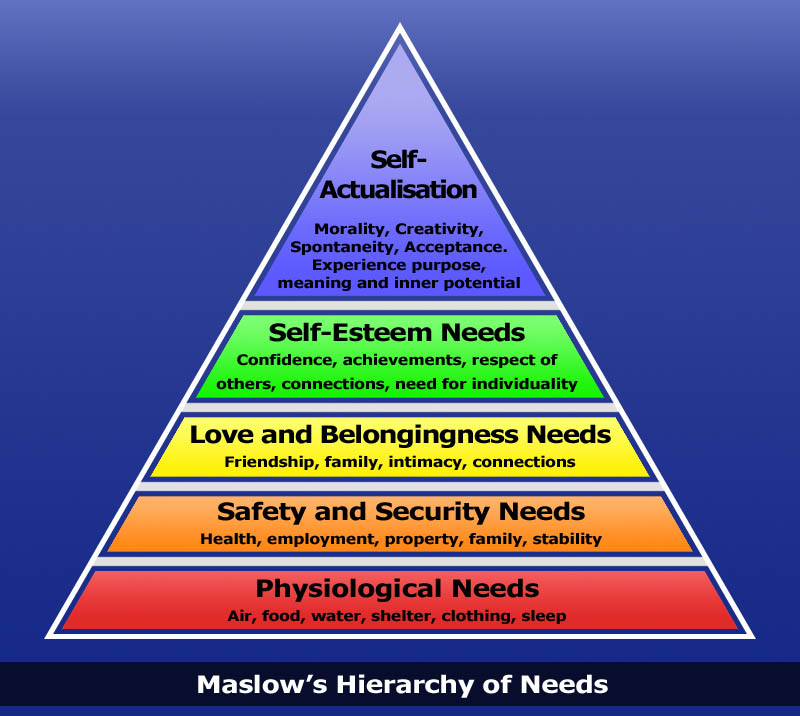

Ball park – you also need to grasp human needs. Let’s go to psych 101 and talk about Maslow’s hierarchy of needs.

At the very basic level, you are talking air, then water, then food. Maybe the next level is dealing with shelter – and even hygiene and protection from COVID these days. Social may be groups – if you are all by yourself, it’s hard to take care of all needs, but with a group, you might be able to have division of labor, specialization, and security needs. Esteem and self actualization I might leave out of this book because this would be one more for survival, and not so much making you feel good about yourself. However – for the sake of this book, creating some sort of plan and preparing COULD perhaps help you sleep better.

Let me explain one concept. I feel there is a high probability of a once in a 100 year financial event about to occur. I could be 100% wrong, and the “1,000 PhDs” at the Fed may think their way out of this. I WANT to be wrong. But I do not believe the government is to think for the good of 300m individuals, but for the good of a nation. Sometimes, what might be good for a nation may counter what is good for my family. Therefore, I believe each individual CAN hope there is a great plan in the works with our central bank, but concurrently also looking at what is best for their individual family as well. The same people that mandate you to pay money for house insurance and car insurance to protect those assets, have not provided you any tools or game plan on how to insure your FAMILY.

The goal of this would be to help people protect their families with a unique form of insurance plan. I would also re-write maslow’s needs to more or less have a core with layers of an onion. For example, you hear Doug Casey talk about having bank accounts in other countries. How practical is that for 90% of Americans? I’m probably somewhere in the top 5-10% of earners and I have zero clue how I’d even go about getting a bank account in another country. For those 90% of Americans, I’m not sure they would even have a clue how to fund it. I’d say a situation like this would be on an outer layer of the onion, and be most applicable towards those with excessive wealth to preserve. For most of us, though, we’d need a practical guide on how to store food, how to keep the lights on, etc.

This is how an example of what an IT manager might look at for threats.

How would a family then see the threats? This is an example – as the threats (big problems) would be laid out in section one. For instance – in a credit crunch, perhaps water facilities stop providing water? I know in Venezuela they only have power rationed a few hours a week.

Section 2 would then discuss what you can do about these threats. Give ideas. Costs. How to prioritize. For example, above you saw me put “moderate” for loss of power and to “accept”. Right now, my primary focus is saving cash and storing food/water. However, as time permits, I’d like to get one of those generators that hooks into your gas line and flips over in the event of a power loss.

Something also not mentioned here is health. Not going to get into it too much, as I have 140 health blogs here on my site, but my PERSONAL BELIEFS are that my personal health is optimized by two things:

- Preventing obesity

- Reduce/eliminate inflammatory foods.

I feel the above 2 items are the root of most disease in the world. MY personal plan could have a threat on there of COVID and how to mitigate it would be to stay in shape and eat grass fed/organic foods, when possible. I should not be talking now, as I put on the COVID 40, but the idea here is that each risk management plan would be different for each family. Holter kind of illustrated the point that is makes no sense if you have $10,000 in cash and stacks of gold and silver if your electric goes out due to the credit system collapsing. While I do not have a farm, I do have connections to get grass fed, grass finished beef for a fee. Those with a farm or land may have a different plan than me. Perhaps one of their plans is to be a provider of goods – in which case security for them may be a higher priority than mine.

Section 3 could be about the different scenarios, and how they could play out. In IT, one of my concerns from a macro level is something called a Carrington Event – where it’s possible all IT systems could be fried. Power grid could go down for a year or more. If power goes down, how are you charging your EVs? Gas powered cars work, for a time, but they you may have problem pumping gas or supplying it, because how is anyone doing transactions? At the root of that cluster then is farm equipment and food production. If you are in colder climates, then you worry about heat in winter.

The idea is in section 3 some concepts of how some things could play out could give people ideas on how to put their framework together. I don’t think you need to be a prepper here – but even some sort of 2 week supply of food and water could go a long way towards hardening you against many shorter term events.

Section 3 could also cover concepts like what happens if the BRICS+16 countries start trading in gold, and have currency backed by gold. What happens to the G20 or so nations that are all paper fiat? Would the BRICS+16 nations even supply goods and services for worthless paper??? In section 1, we could discuss at length the concept of MMT – but you have many older nations that don’t back that. And, in section 3 – hypothetically speaking – does world war 3 break out between nations that use gold-backed currencies versus those that use paper-only? Would it be a cold war of sorts first? Could this type of scenario then allow mining for the 70m ounces of gold at Northern Dynasty? How could hyper inflation of commodities prices affect the green new deal with silver as a primary metal of this? Section 3 could go over the different scenarios in front of us – David Hunter’s global bust, Brent Johnson’s dollar milkshake, Harry Dent’s deflation, Peter Schiff’s dollar collapse, Jim Rickard’s “The New Great Depression”, and Maloney’s currency debasement and money bombers with us going Weimar. David Morgan and David Smith discussing silver’s major move up and how to capitalize on it? Each of these scenarios may have an element of gold and silver in there for protection, but what specifically could you do for each scenario to protect yourself? Is any of this discussed in Anti-Fragile? I don’t read enough books. I have gotten 3/4ths through Maloney’s, then watched the series a dozen times. I got about halfway through Morgan/Smith’s book, and I have Rickard’s book on my desk here staring at me for 2 months.

Hardening myself….

In IT security, one concept is finding threats and risks and “hardening” the systems from attack. I feel in this financial turmoil situation, we must all “financially harden” ourselves.

I heard a quote from Dave Ramsey a few years ago and my wife now hates me for it. “We buy things we don’t need with money we don’t have to impress people we don’t like”. So, in a lot of respects, I just don’t give a @#%% about trying to impress you with things. That ship sailed years ago. I have a coffee cup I got on my honeymoon 8 years ago, and I use it every day. I will for the rest of my life or until it breaks. Certain things mean something to me. But I don’t need to go out and buy a coffee cup set for $100 for the possibility of having company in 1-2 years when the ‘Rona passes. Just don’t care. Deal. And that is the attitude many people need to adopt, and very soon. Spend money, but in the right places. Skip a vacation for a year or two and bolster your savings and invest in your home and food stocks. Learn a new skill or trade. Go without for a short time and invest in your family.

My primary focus at this moment has been to harden myself and my family against impending doom and my wife busts my chops over a new kitchen table. These are real life things we must all deal with, every day. We can’t just curl up in a ball and buy hundreds of pounds of rice and ignore daily needs. I have to chairs that are broken and the table is a mess. So, ok, she won that round. But do I need a $3,000 kitchen table? No. I want to get something practical and inexpensive. IF we all make it through this shit show in 5 years, then ok, maybe I really up my game with some furniture. While this is NOT financial advice, I personally have cut my budget significantly over the years to necessities only. Once I feel “good” with my plan, and I have my target savings and feel good – maybe then I unleash hell on some things. But that is the ROOT of our issues today – gross consumerism without respect if you need things, and to what degree you should spend on things no one gives a shit about. Sorry, I just don’t care these days. I have a $47,000 car that is now 4 years old and my new game plan is to drive it until it literally falls apart in 2045. Maybe I get a pick up truck at some point for hauling. I don’t really see myself ever buying a new car again.

One thing that I have done over the years is to try and envision a day when my career goes away – what happens? Everyone reading this should be thinking the same thing. Whether by force, or by choice – what happens if my career is gone? I’m working my dream job now, but it’s also 90 minutes from my house. What if bad things happen globally and I have to take a job that pays half as much? I have done things over the years to try and harden myself against this stuff. I now own 3 houses as a real estate investor – 2 I rent out (3 units), and I live in 1 – Worst case I could sell all three of them and rent somewhere? Maybe I buy a few more with miners profits? I have an MBA to complement my IT background, so if I have to leave IT, I could in another field as a manager. I have a Project Management Professional certification, which is a skill than transcends IT and maybe I could get into house building project management. I haven’t been great with my hands, so I took on re-doing my unfinished basement and have now drywalled, mudded, framed out walls, done drop ceilings, installed flooring, painted – and put a gym in – so I could work as a day laborer if needed. I write a ton, and perhaps that leads to a second or 5th source of income someday. I spent many years working with fitness and may someday want to pursue a career in helping people lose weight (I lost 175 pounds) and preventing disease (both of my parents died of cancer so I’m passionate about prevention). I played in orchestras and could perhaps work side gigs playing my trumpet for $25-$50. I competed at the world level for chess as a teenager, and maybe I could play small tournaments for grocery money for the family. I started a garden and grew tons of cherry tomatoes and raspberries, and look to grow my garden more this year to add more value-maybe I could exchange piles of fruits/veggies for chickens or eggs. I have been extremely active with investing and mining stocks, and doubled my pile in the metals/mining stocks in 10 months. I learned how to shoot guns and was an avid fisherman growing up, so I feel I could hunt/fish if need be. A few years ago, I even tried to get a Direct Commission as an officer into the Army/Navy for cybersecurity (I have advanced degrees, certifications, and experience in this sector) to make some side money and pay off student loans, but that didn’t pan out as I’d hoped. I now have a 9 month old and I’m 45, so that’s off the table.

What you see above is that I am trying to constantly find more ways I can provide value to others to protect my family and improve myself. Hence the “renaissance man” part of this site name. No, I’m not wielding swords as a renaissance fair. We live in a cruel world. If our primary means of providing value is stripped from us, do we shrug our shoulders and wait for the government to solve our problems? I lived through several layoffs, including a 15 month layoff at the end of the dot com era – and I told myself I’d never let that happen to me again. Since 2003, the longest I’ve been out of work has been 8 days, in a HIGHLY volatile career field.

We have lived in the most entitled nation in history, and a vast majority of us have never seen the horrors that much of the rest of the world has seen. We take this life for granted, and it’s so easy to avoid thinking about the unpleasant nature of if things go sideways. We tend to think of The Great Depression as a yard stick for this, but many have not taken this a step further – what happens if our government is insolvent during the next great depression? Has it already started September 16th, 2019 and so far the issues have just been painted over? Will we look back 20 years from now and see how this was the early stages already? Or – has the main event not happened yet and could be delayed until 2030?

Someone like me hopes I’m wrong about believing all of these guys. The spidey sense in me feels each of them are right, to varying degrees, and because of this, I feel a duty to have to protect my family. I feel a duty to protect them over getting a new (enter frivolous shit here). And, my urgency in this matter will remain so until I feel we are in a good place.

For our car insurance, we write a $50 check each month. For our family’s insurance, it requires a lot more effort than just writing a check. And – this requires some sacrifice. My 94 year old grandmother is a Great Depression survivor. Canned food for years. They had a massive garden. She would even carefully open presents and re-use the wrapping paper. We buy shit without looking at price tags, buy people excessive gifts they don’t need, and might pay a little extra for creative wrapping paper that’s ripped apart and cards that cost $7 that no one keeps. There are lessons we can use to conserve these resources. Once we put together this risk plan and execute – perhaps THEN we can return to some more consumerism? I feel right now, this country spends first, shit goes sideways, then expects the government to support them. I feel everyone has a duty to create their own backup plans – and the government is the emergency backstop of last resort, not first resort.

I haven’t read the book Anti-fragile by Nassim Talib, I heard Rick Rule discuss it several times. I think I have felt something wrong the last 4 years or so, and I’m looking to get myself to be “anti-fragile”. It’s on my list to find, buy, and read – but again, there’s that time thing going on here I don’t have.

I’d love a book I’m describing like the above, and hell, I might write it someday as a 9th source of income if I ever have the time. I’m finishing up the gym now and plan to spend the next 4-6 months taking off the COVID 40, then getting back in to running, biking, and perhaps do a triathlon in August. I wish there were 40 hours in a day!!

P.S. When I learned about a lot of the repo market issues, I wrote a ton more about this subject about 15-16 months ago. Here’s a few of those if you are so inclined. Some of them were more geared towards getting some physical silver and getting your food pantry prepped. Check out December 2019/January 2020

December 2019 – Renaissancemen.org

March 7, 2021 at 4:54 pm

Good afternoon, as always, it is a pleasure to read to you, my family since the COVID thing changed the way we think and act. Apart from working both in good jobs, we make gardens that we sell what we have left over or we exchange cultivating land with olive trees and we make organic oil which we also sell the surpluses. We buy physical gold silver every month and we have begun to invest the mining companies. love the change of life to us and our children, thank you for your writings.

March 10, 2021 at 8:27 am

Reading this was just lovely 🙂