Summary: This is a former silver-miner-turned-junior gold miner with 500k AuEq oz by next summer with diversified assets in many countries. It is significantly undervalued to its peers, and with a potential for $2200-$2500 gold price inside of 12-18 months, I will demonstrate how any investment now and holding until then could have an investor return 6x and have this junior gold producer have returns like a high-risk explorer.

If you want to skip the back story as to WHY many silver producers are now moving to more gold production, go right to ‘FSM deep dive’ section.

Background of primary silver producers and why they are adding gold to their production

I’ve been writing a lot of cheerleading posts about Fortuna Silver Mines lately. Disclaimer – I am HEAVILY invested in them (for a good reason you will see here) so I am biased, but I’m heavily invested in them BECAUSE they are so undervalued. My articles here are to point out that I feel FSM is SIGNIFICANTLY undervalued to its peers. But, who are its peers? Funny I should ask that. Fortuna SILVER mines, right? Well, as it turns out, they only produce about 27% silver now. It’s more gold than silver. With a new gold mine starting in The Ivory Coast next summer, it will be even more percentage gold than now.

I have written articles about how the silver manipulated price seems to be putting a lot of pressure on primary silver producers. That is, most production of silver is a byproduct of other metals. For example, I had done some calculations and found that Newmont produces about 54m oz of silver a year. IF they were a primary silver producer, it would make them either the largest or second largest. Then you have a lot of base metal companies producing silver and silver credits help increase their profitability for zinc, lead, etc. Meaning – for 90% of the miners out there, the price of silver is relatively immaterial to their primary business. Sure, it helps with profitability, but whether silver is $30 or $15 makes little difference to their OVERALL business.

Which is why the futures is important, to an extent. The futures market essentially creates efficiencies with commodities. While it’s hard to describe without complex math, you can see downtrends in commodities prices versus inflation over a very long period of time. Meaning, while you have decreasing ore grades, you may have more efficient means of production with better and more modern equipment to drive down coasts (like First Majestic’s HIG mill). Those who can produce at these levels keep the lights on. Those who cannot, exit the industry. Eventually, if production dips too low, price moves up to entice more to produce.

I believe over the next few years, silver price is to go bananas. Those micro juniors that still exist – will either be bought out by a First Majestic needing to replenish ounces or print money if they can hang on until then.

With silver, it’s a VERY interesting problem outside of gold. Gold has primary producers that make bank. However, silver primary producers produce perhaps 12% of all silver. That is to say, that price can continue sideways indefinitely, UNTIL production dips far enough below demand where price needs to rise. Unlike cattle or hogs where you can just…make more in short time…silver primary miners have been under-budgeted for a decade, and exploration has been slow to catch up. This has led to a situation where the byproduct producers of silver cannot just dial up supply – and gradually, then suddenly, we can see silver primary producers fall into the abyss. To me, this moment of “oh shit” is going to be worth all of the pain and suffering we all have encountered over the last 18 months. The time I believe for this moment is inside of 5 years. You can clearly see the supply/demand cracks forming – and this will be similar to what happens when an earthquake happens. Tectonic plates are colliding, and most investors are fat, drunk, and stupid to just see silver at $23-$27, hoping for $50, and not completely understanding the major forces at work far below the surface. I do.

Until then, what is happening? You are seeing silver companies like Fortuna Silver Mines, Pan American, and First Majestic all take on gold to keep the lights on. I believe Endeavor now is 60/40 silver to gold. I believe Fortuna is a 27% silver producer, PAAS at 26%, and AG at 50% (they say 55%-60%, but with Jerrit Canyon, I had read multiple sources it is closer to 50%). The point here is strong silver companies are getting squeezed out and can see that unless they take on gold mines for profitability, the lights will go out inside 5-10 years. Remember, for every ounce they produce, they have to perhaps not only find another to replace it, but even another to grow their company.

IF and WHEN silver tectonic plates collide, those with the largest exposure to silver will hit the lottery. This is why a First Majestic just doesn’t switch over everything to gold. Gold pays the bills, but silver is that lottery ticket. Consider many are thinking that in the next few years, gold has a potential to move to $2200-$3000. From $1800 now, it’s a good move, but consider a Discovery metals with 600m oz of silver who could see a silver price inside of 5 years go from $23 to $100 or more. Meaning, exposure to silver IS important, but it’s harder and harder for a silver primary producer to be profitable with these ore grades at $22 silver. Taj Singh was banking on Discovery to be a “home run” over $20 silver. But at $22, you don’t have incredible margins – but at $50 to $100? Dear God.

But isn’t there infinite levels of silver out there? Not quite. While we have found 60b oz already, it is getting harder and harder to find silver, meaning one of two things will happen:

- No silver from primary producers to leave us at a 12% deficit yearly in an increasingly high demand of silver society

- Price goes up to support the 12% silver production that primary producers produce.

My Twitter friend Mr. Billy B., who has a striking resemblance to Leslie Nielsen (lol) posted the below picture the other day. I found it fascinating. This is why I’m on Twitter a lot. Great stuff to learn!

When you zoom in on metals, you see this…

This shows that in the earth, overall, silver is found at almost 2:1 of gold. Over 5000 years, it was found and priced at 15:1. My guess is more silver was closer to the surface, easier to mine, and that the rate at which they found it. Keith Neumeyer has repeated many times that they are finding it at 9:1 and 8:1. I believe he even once said 7:1, but don’t quote me on that. That is, to say that finding silver may now be getting more difficult. And more expensive, meaning that most of the near surface silver has been mined.

Now, platinum is something like 30x more rare than gold, but actually just over half the price of it. Many people (like my hard money bitcoiner friends) like to point out that scarce supply makes something valuable. Scarcity alone, sadly, does not. IF true, then why is platinum not 30x the price of gold? Why isn’t gold only 8x more valuable than silver? The truth is, people who tell you something is valuable because it is scarce need to go back to day one of economics where you discuss supply AND demand. Meaning, my kid’s fingerpainting from his daycare is a one-of-a-kind masterpiece. But, if no one WANTS it, and there s ZERO demand for it (business case) then it is worthless. The quantity of supply ONLY matters when demand is factored in. For my bitcoiner friends, you need to let this really sink in, and really understand why Saylor hypes the demand side at all times. I digress…

While many of my friends are in on platinum, I am not. Historically, platinum has a much better ratio to gold, but it’s primarily used in catalytic converters. In MY world, in the next 10 years EVs are taking over everything, and with that, the demand for catalytic converters will go way down. I know, I know – diesel and standard, and they may use more platinum outside of diesel as it is cheaper than palladium. However, I feel the who ICE thing is coming to an end. Again – slowly, then suddenly. In the near term investment in platinum may decay and this could reveal a platinum to gold ratio that spikes – but it’s a guess here of throwing darts for an element that has one major commercial use. I’m not anti-platinum, but I’m more pro-gold and pro-silver and I only have so much plasma to sell to buy in to these things.

The point here then is – silver is hard to find, and half as rare as gold. But, the DEMAND for silver is increasing. Silver wears two hats, both as money and as an industrial metal. There are people like Lobo Tiggre who say silver is dead as money because now you can slice up gold on a blockchain. I am HEAVILY invested in Kinesis, and agree – to an extent. Just because I have money in digits in a bank, doesn’t mean I don’t have some cash at home for emergencies in case the banking system has a problem. And, I see that same thing here with silver where people who believe in sound money ALSO want money in their hands, and gold is too dense of a store of wealth for most people. I feel gold will eventually move to replace the dollar as international currency so countries can settle in gold, perhaps on the blockchain in vaults in neutral countries – but silver I believe will ALWAYS be the money of the people, in hand. So I do not see stackers one day just handing over their stacks for digital numbers saying you own so many salami slices of gold on the blockchain. Not happening.

Consider Russia now facing a SWIFT ban. Russia has thousands of tons of gold. So do many BRICS+16 countries now. If the US is using SWIFT as a punishment, it potentially means a country with the reserve currency of the world is then using this to shape a world that suits them. I live in the US, love my country, wave my flag – but those who are monetary experts will tell you that if a country abuses the right of the reserve currency, other countries may challenge that hegemony. Consider Russia, with lots of gold, deposits into a third party vault, like Switzerland or Kinesis. Consider the Germans do the same. Germany, China, Indonesia – can buy gold in their currency and then buy Russian natural gas or oil in gold. Russia can then take possession of that gold in these vaults, and turn around and sell gold for Rubles or Yuan or US dollars. Meaning – gold could become the international currency to buy commodities to replace the US dollar as a reserve currency. Now that blockchains are a thing, and vaults are literally all over the world, it’s very easy to decentralize all gold holdings into dozens or hundreds of vaults and then do commerce with this gold and blockchain. Anyway – the point is here that Lobo is on the right track with gold, and I can see how belligerent countries to US foreign policy can simply buy and sell commodities in gold, given that most countries over the last 20 years have boosted their gold reserves.

The demand for silver as money/investment is increasing, as evidenced by ETF hoarding – but also as an industrial component in such things as EVs and solar. Unlike gold, however, a lot of the mined silver ends up trapped in goods that are not recoverable for less than $75 per ounce prices. This is different than SCRAP, where we are talking about sterling, jewelry, and constitutional silver (90%) being melted down to make .999 fine bars for industrial usage. What is interesting, is that we are scrapping 150-200m oz per year, but the sources of that scrap are resulting in 220-250m in goods (meaning scrap is running at a deficit). So – I believe we have a MASSIVE stockpile available to us at $75 silver – when we burn through all available AT THIS PRICE and mining production cannot keep up with demand. However, the companies and processes are NOT there to recycle millions of ounces of silver – so there could be a violent upswing past $75 to get these companies spun up. After that, you will see potentially price come back to $75 for some time. But the costs of recycling will also go up over time – as it becomes harder to source material and the “easy” stuff to recover has been recovered. This, as energy prices go up and silver ore grades continually decline with no ounces being discovered to replace those being mined now.

FSM deep dive

I bring all of this up as a backdrop to look at FSM and how a company like this with exposure to gold and silver can just go crazy. They were primarily a silver company who have taken on gold assets. Same with PAAS. Same with First Majestic. To me, the mid-tier companies like this will need to adopt gold in order to survive. Some of First Majestic’s mines they had put on care and maintenance had high twenties into the $30s for AISC. How can you produce silver at a cost to you of $35 when price is $23? you cannot. But when price is back over $40, they can fire it back up, to help a little more with supply. I believe, however, none of these companies can dial up production to meet the avalanche of demand.

With that – I wanted to look at FSM and how it is trading. Basically, I have seen it get smashed when the environmental permit was threatened, and not recover where it was, even though the threat has passed. I wanted to look at where it was trading – and I consider PAAS its closest peer in type of production. I will also use First Majestic as a silver comparison. But I also wanted to compare FSM to Newmont given it is a majority gold producer.

Here’s what I found. It is severely undervalued to its peers. To me, this is obvious. Everyone knows about the permitting problem, but many don’t know prices were later smashed for the whole industry, and when a recovery sort of happened – it was the same time the permit was re-instated and FSM never recovered to where it was prior to this.

Check this…

Is FSM a gold company?

In the last 973 days or so, you can see gold rise 45%. Newmont rose 86% (about double), Barrick 61% (1.5x), and PAAS at 95% (trades like a gold junior). FSM, however, is only up 31% – underperforming the metal’s rise.

So maybe it’s trading like a silver company?

You can see over that same period of time, silver is up 39%. First Majestic up 51%, Endeavor silver up 23%, and PAAS up 34%. FSM? -39% to silver price.

Part of this whole thing I believe is identity crisis. As it is less of a silver stock, those wanting silver exposure are going for First Majestic and Endeavor. Those wanting more gold exposure see “silver” in the name and don’t see it as a gold stock. So, part of me thinks Fortuna might need to rebrand in the next 6 months or share price can linger. How about, “Fortuna Gold and Silver”? Change the ticker. Part of me also wants them to buy out America’s Gold and Silver (USAS) to then move up the America’s for a very geographically diverse company running both gold and silver, and they could probably buy our USAS at a discount. USAS has assets of $286m on their balance sheet with a market cap of $119m. You tell me what company is more ripe for a takeover target with good assets that were mismanaged?

Now, I’m very much aware that the permitting situation with FSM negatively affected price. But let’s say, for argument’s sake, that gold and silver trade sideways for another year in a tight channel. All things being equal, you can pretty much tell that value will be found with FSM to get it back up to its peers. Meaning – just by trading sideways, it is easy to see FSM will outperform its peers as news of the permitting is in the rear view mirror and people take a second look to find value.

Well, let’s take a look quick at their books. I did a study on silver miners – based SOLELY on their books, and then placed FSM 5th out of 13th. At issue with FSM to me was jurisdictional issues and a large amount of debt – but their P/E ratio was actually a great bargain. The debt though, looked to be towards constructing a mine at the Ivory Coast over the next 18 months, so that’s going to pay itself back nicely. Take a look…

Yahoo always puts miners as “overvalued”, but more important, take a look at the low price to earnings ratio. There are a lot of ways to measure companies, but this to me is the first thing I look at before I dig deeper. I’d say most are looking to be 12-20x. When you are on the low end of this, your share price is unloved. It could be the CEO is not marketing the company enough. It could be a discount for the mining jurisdictions I talked about (Peru, Argentina, Mexico, Burkina Faso, and Ivory Coast). Of the jurisdictions, I felt Mexico was the safest. Well, we now have a coup in Burkina Faso – but apparently coups in Africa aren’t all that uncommon. More on jurisdictions below.

Now – how about it’s peers I’m talking about here? Let’s look at each…

PAAS – 19x

AG – 72.93x

NEM – 24.32x

EXK – 18x

By these rough numbers, you can potentially see FSM P/E undervalued to its peers by 1.5-2x. Remember that. Currently, today’s price of FSM is $3.46. Take that time 1.5 and you get $5.19. Take it times 2, you get $6.92. Now, I arrive at this same price below by looking at the price of gold.

On this chart, you can see FSM share price in green circles at $1844 or above. What you can see is that the last time gold was $1844, the share price was $5.52. The time before that, it was in a trading range between $6 and $8 ($7 avg), and that was BEFORE the Roxgold mines were taken over.

I have actually found that Fortuna is trading as if the gold price, TODAY was $1250-$1500. Don’t believe me? Let’s look back to 2019.

Or – we can take a look back and show that FSM was $9.73 on $1366 gold in 2016. And at $3.30 today at $1800. I’m aware share dilution could have a big part in that, but still. Look at that ascent from $2 to $9 in a few months???

I have read Dave Kranzler comparing FSM’s gold production profile to others. He pointed to FSM’s future production profile of 400-500k AuEq oz to Alamos gold’s – and pointed out that Alamos has a $3b market cap. So while I can’t take credit for that research – I can cite the source for it and I can review the company presentation slides to show this (below graphic). Their corporate presentation has 326k-371k AuEq oz with the Ivory Coast project in construction now for first pour mid 2023.

It appears that a market peer to FSM’s is trading at 3x the market cap of FSM. Now – to be fair, you could make the argument that Alamos is overvalued. At THIS point, with the tax loss selling and multiple smashes in metals, it’s really hard to find companies now OVER valued. What I’m looking for at the moment is those MOST undervalued to peers, and FSM is up there at the top. Now, the Ivory Coast mine is slated to mine about 150k AuEq oz per year – which will take FSM more more skewed towards a gold producer. This would indicate to me it might be treated like a Jr. gold producer for GDXJ. And there it is…

And – part of GDX.

What I’d expect with institutional holdings would be to see how undervalued it is – with production increasing by 20% or so could have these holdings significantly increase relative to other holdings in the funds.

Lastly – take a look at their balance sheet. If you just looked at their total assets, you see $1.055B.

Their market cap is $956m. I am seeing $12m in FCF the TTM, but you can see 85% of their free cash went to investing activities in PPE, such as building a mine, equipment, etc – building value in the overall company. If you simply sold it for spare parts, today, your share price is higher. Let that sink in. That completely discounts all future FCF. BARGAIN!!!!

If you did this same exercise for First Majestic, you have…$1.23b in assets to a $2.5b market cap. About double a market cap for the assets.

With First Majestic, you also see $22m operating cash flow, but -$142m in FCF. This to me shows FSM is using cash on hand to grow organically and put sales into the ground and not take on more debt or do share dilution.

Now, let’s look at PAAS – which is similar in silver/gold production profile, but I think PAAS has more base metals.

PAAS has a mkt cap of $4.6b with $3.4b in assets, with $217m FCF. They also have $160m in investment activities, but have a superior FCF.

PAAS is also undervalued, and has taken a ding on jurisdiction issues. But, you can see that comparing to its peers, you have FCF models in mining all over the place based a lot on how you acquire assets, buy equipment, and put the money back into more producing mines to replace the ounces mined.

To recap:

- FSM more closely trades with gold and has underperformed the price of gold. It may have branding issues, at this point, which can be resolved.

- FSM trades at around a 33-50% discount to its peers with P/E ratio as a measure

- Its market cap is less than its assets. It completely discounts future FCF.

- FSM has debt to build a mine, but operates with positive FCF.

- FSM price at $1844 gold is down about $1.50-$3 from the last few times gold was priced at this level

- FSM is currently priced as if gold was $1250-$1500.

- Since the green channel above, they took 2 good Roxgold assets on, including a producing gold mine. Also since then, Lindero has ramped up gold production and will churn out over 100k AuEq oz this year.

- A new mine is coming online in 18 months in the Ivory Coast to produce another 150k in AuEq oz which should lead to a re-rate of the stock.

- Jurisdiction problems in Mexico were resolved, but new issues popped up in Burkina Faso that appear to not affect mining operations. See below.

- FSM is included in major gold mining indices. With Lindero ramping up and the Ivory Coast project being built, my expectations are major funds will allocate a greater portion to them – boosting share prices.

I believe, today, FSM is a $7 stock trading at $3.44, on its way to a $10 stock re-rate if gold price remains the same (re-rate to Alamos level as gold production gets to 400-500k AuEq oz). Essentially, every share I buy, I am under the belief someone is handing me nearly $7 in cash that I can redeem over the summer or this coming fall. I have accumulated as much as I can, and used call options where I could to ramp up my leverage to this.

When gold prices ramp up to perhaps $2200-$2500 per ounce, the expectation is GDX and GDXJ will go bananas, and with this, you could potentially see the GDX/GDXJ move up 50-100% – and all of their allocations in these stocks double. If I’m thinking FSM is a $10 stock this summer, at current gold prices, that then potentially projects to a $15-$20 stock with $2200-$2500 gold. Maybe it’s a bit on the high end, but if we are at $2500 gold, all bets are off for anything as these stocks may trade like tech stocks.

I’m paying $3.30 today to buy more. I’m banking on a $2200-$2500 gold price by end of year or in 2023 to get me potentially a 6x return. I will take that every day and ask for more, please. This is having a mid-tier producer potentially having the returns of a high risk explorer. When the light bulb goes off for most of you, I might be at 20,000-30,000 shares. I have made this a major portion of my trading fund. While it is very smart to diversify, I cannot overlook how this could be a 3x if simply marketed at fair value to its peers.

Jurisdiction

One thing that made me have SOME hesitation with Fortuna was jurisdiction. Of all of the places they operated, I felt Mexico was by far the best. My entire thinking of jurisdiction is now changing. Look at how Mexico has a $200m tax issue hanging over First Majestic?

Peru – had some issues with new president and anti-mining. Crushed Peru stocks. Replaced person and softened tone, mining stocks started recovering.

Chile – young president elected who appears to be anti-mining.

USA – environment. Look at Northern Dynasty. Take a look at California versus Nevada, night and day. Very leftist president has shut down a lot of resource exploration with oil. Could they clamp down more on permits for gold/silver?

Canada – very friendly

Australia – very friendly

Africa – seems all kinds of problems. Africa has a TON of resources, and is the size of N America AND S America in one. The major issue you see is “rule of law”. If you cannot have stability with governments and laws, how do you have investment? I know the Chinese are eying Africa – but I think many are looking there now for sources of selling goods and services to. But they need to build revenue and infrastructure, and mining may be the entire backbone of Africa’s awakening. Just like the USA, there are many different types of jurisdictions.

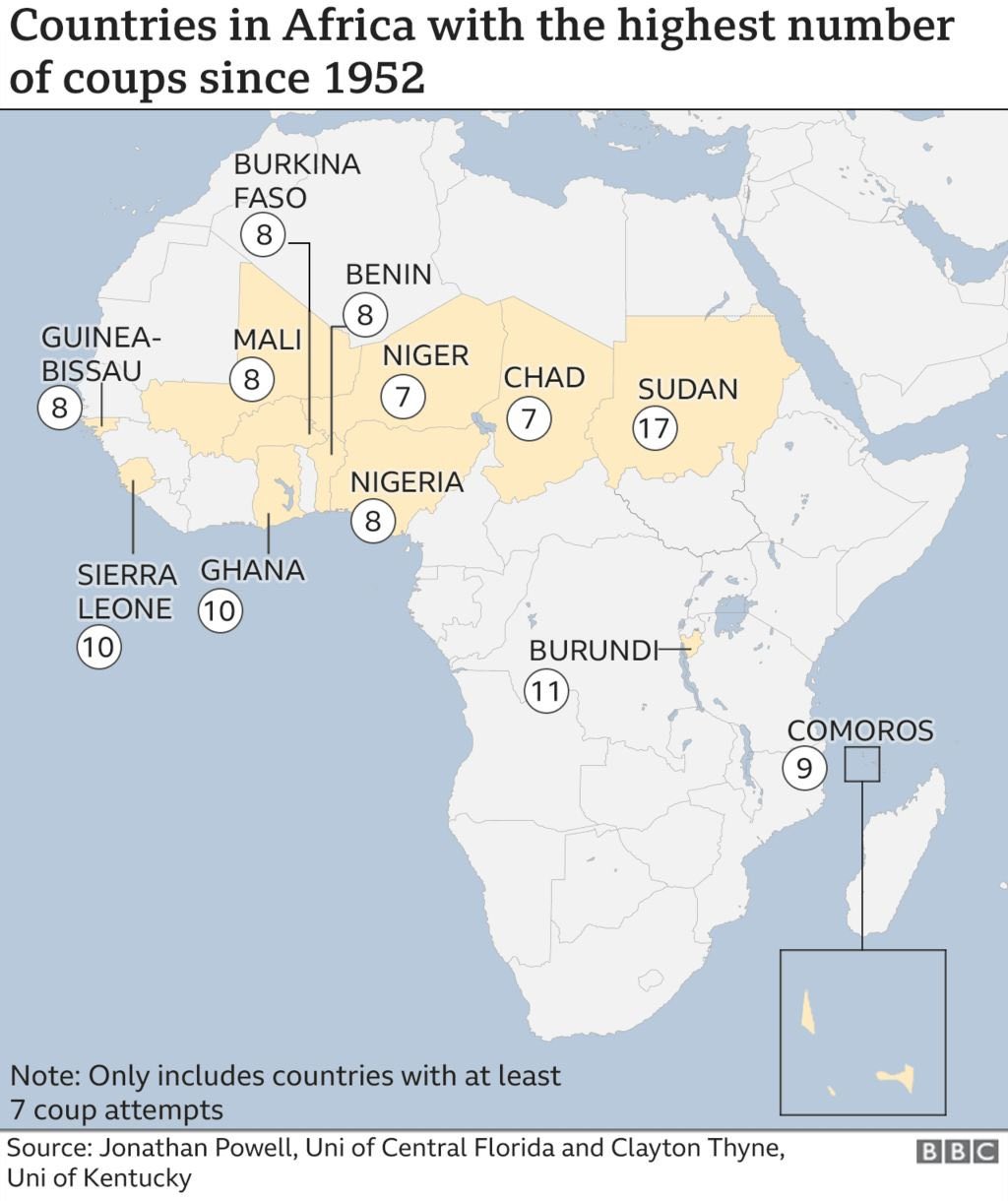

I saw this chart on Twitter and it made me sad….

The first thing you do is search this for the highest number. Then look down over the next highest, etc. at the very bottom, there’s a note that has SEVEN coup attempts as the cutoff. Sorry, if you have 6, you didn’t make the cut.

When I made a comment the other day about how the coup in Burkina Faso didn’t seem to affect FSM, I think I was a bit insensitive unintentionally. To us in the US, we just see instability in Africa as a constant – and while sad, it’s a fact of investment reality. The truth is, there are people in these nations severely affected by these coups, and I feel for them. I just figured it was a handful of nations with a few attempts. I didn’t realize how widespread this was, and how often it happened. Shocking to me.

But this then brought up my reservations with FSM. Is Burkina Faso safe? Another ding to the stocks, but when you hear from those who are there, you hear that the government was corrupt and the people in general supported this move to reduce the corruption. The truth is, you have to say for many of these stocks, “it depends”. It’s partly why gold stocks get beaten down on. They operate in some tough jurisdictions with unclear business impediments like permitting, strikes, and natural disasters.

You then have the mine in the Ivory Coast (one of the exploration projects) which posted this result last week – which is REALLY good. So they have mines now in Peru, Mexico, Argentina, Burkina Faso – and in 18 months or so, this exploration to a nearby mine to start. The construction decision was made, and now we wait.

Conclusion

To me, it is clear we will need a LOT of silver upcoming. It is also clear to me that gold may play a part in international currencies as a single nation’s currency may not be the longer term solution to a reserve currency – and gold could even get re-priced in the years ahead. Many talk about a “basket” of currencies, but these are all worthless pieces of paper. Most central banks are holding gold now, and you can even see many getting away from the USD and favoring gold. In this scenario, I am a big believer in silver as an industrial metal and gold as a monetary metal. Fortuna Silver miners mines both of these precious metals and is increasing their gold production as we speak to ramp up to about half a million AuEq oz per year by next summer.

If I am to invest in silver miners – and gold miners – I want the most torque possible AND the best miners WITH the best teams IN the best jurisdictions. I believe the Roxgold acquisition to increase FSMs gold production and diversify their mining jurisdictions was masterful. Their debt they hold is going into the ground to make more money from it. I believe FSMs jurisdictions are challenging, but this is the environment for most miners today. The company has seen its challenges and has rebounded strongly from them.

With all being said, I have shown in several different ways how FSM is essentially paying you cash money to take their stock. To me, it’s a matter of time until analysts see how beaten down this is relative to its peers and when it moves, it will move quickly to catch up.

In Jorge I trust.

January 28, 2022 at 3:35 pm

I agree. That’s why I own 215,000 shares.